Purpose:

To demonstrate how the Depreciation to the Day functionality works in SAP S/4HANA

What will you learn from this Blog post?

From this blog post you can understand

- Calculation of depreciation when the “Depreciation to the day” functionality is active in SAP S/4HANA.

- Special considerations in Leap year vs Non leap year that needs to be factored in for this calculation.

- 8 different scenarios have been explained in this blog post.

Points to be Noted

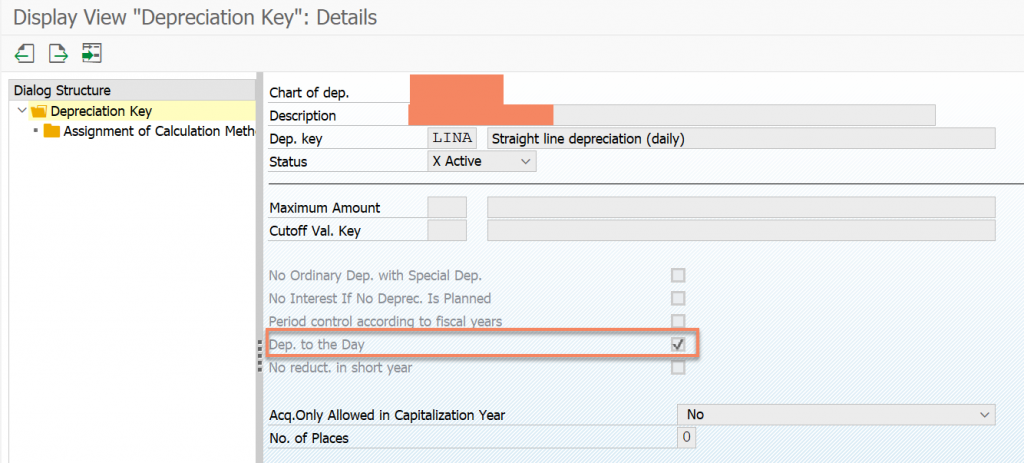

- Period control settings are not applicable when “Depreciation to the Day” is enabled.

- This functionality is useful only with a depreciation key that determines percentage from useful life or from remaining life

- If required, this solution of depreciation to the day can be applied in Cross Sector industries (in any country/industry) where depreciation calculation on a daily basis is required.

- However this function “Depreciation to the day” was released for the country-specific requirements of France and Thailand.

- In case the Net Book Value does not become zero at the end of useful life then use a changeover method in phase 2 for immediate depreciation as shown below.

Depreciation Calculation in SAP S/4HANA:

The depreciation calculation is based on the below factors.

Depreciation = Base Value * Period Factor * Percentage where,

Period Factor = Days to be depreciated in the Year/ Total days in that year

Percentage = Days in the Year / Remaining Useful life

In the blog post below, multiple scenarios have been covered in detail such as Acquisitions with different useful life, Additions to Assets etc. The principle of calculation is same irrespective of the nature of transactions that happen during the asset life cycle (Acquisitions, additions, transfers, retirements etc)

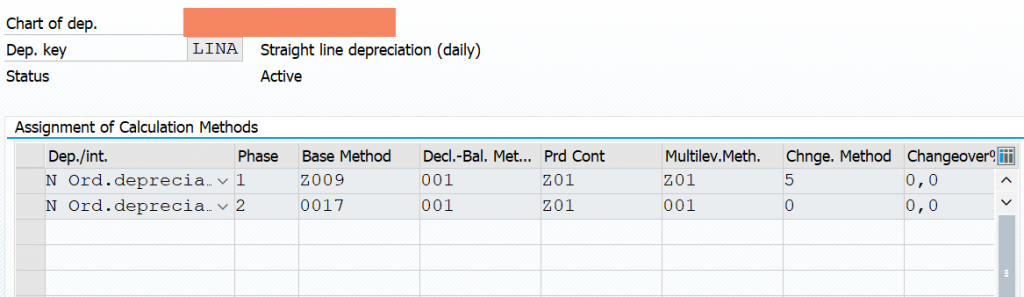

Setup of the Depreciation key

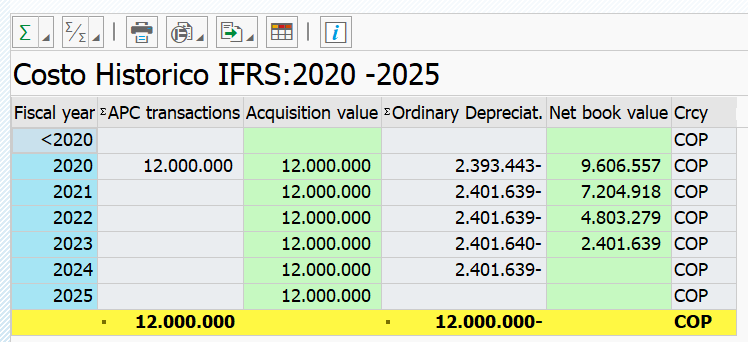

Scenario 1:

Useful Life: 5 Years

Base Method: Percentage from useful life

Depreciation to the Day: Activated

Depreciation start Date: 01/01/2020

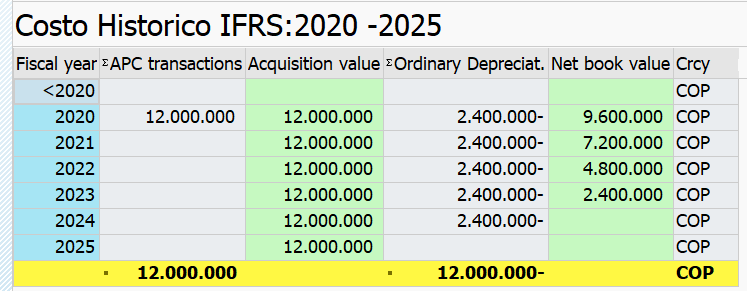

For Year 2020

Period Factor = 366/366 = 1

Percentage = 365/1825

= 0.2

Note:

- Irrespective of 2020 and 2024 being leap year, the system always calculates the Useful life as No of Years * 365. In this case it is 5*365 = 1825

- Leap Year will be considered as normal year in case remaining life is greater than 1 year. So, while calculating percentage it is 365/1825 and not 366/1825.

For Year 2021

Period Factor = 365/365 = 1

Percentage = 365/ (1825-365)

= 365/ 1460

= 0.25

Note: To calculate the remaining useful life I subtracted only 365 from 1825 and not 366 even though 2020 being a leap year. This is because I used only 365 days while calculating the total useful life and SAP S/4HANA normalizes the leap year as 365 days if remaining life is greater than 1 year.

For Year 2022

Period Factor = 365/365 = 1

Percentage = 365/ (1460-365)

= 365/1095

= 0.333

For Year 2023

Period Factor = 365/365 = 1

Percentage = 365/ (1095-365)

= 365/730

= 0.5

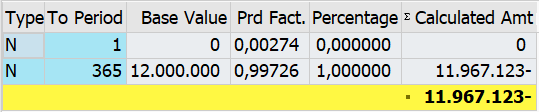

For Year 2024

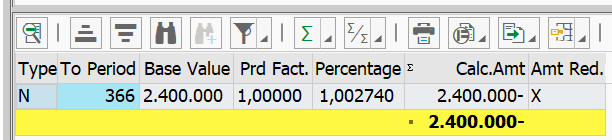

Period Factor = 366/366 = 1

Percentage = 366/365

= 1.002740

Depreciation = Base * Period Factor * Percentage

= 2400000 * 1 * 1.002740

= 2406576

Note:

- Calculated depreciation amount is more than the remaining amount to be depreciated. So, it has activated the “Amount Reduced” flag and made the depreciation amount as 2400000.

- While calculating percentage it has taken 366/365 and not 365/ 365 because the remaining life in 2024 is not more than a year

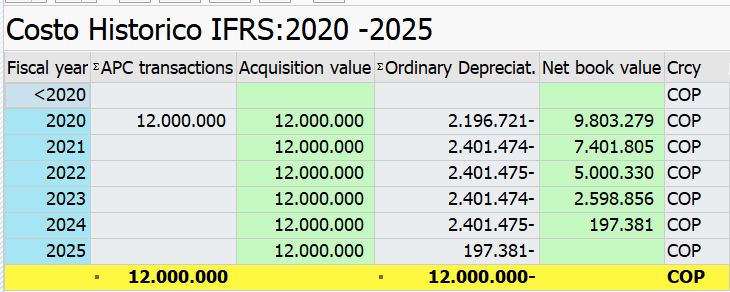

Scenario 2:

Useful Life: 5 Years

Base Method: Percentage from useful life

Depreciation to the Day: Activated

Depreciation start Date: 02/01/2020

For Year 2020

Period Factor = 365/366 = 0.99727

Percentage = 365/1825

= 0.2

Same note mentioned in Scenario 1 applies here

For Year 2021

Period Factor = 365/365 = 1

Percentage = 365/ (1825-365)

= 365/1460

= 0.25

For Year 2022

Period Factor = 365/365 = 1

Percentage = 365/ (1460-365)

= 365/1095

= 0.33

For Year 2023

Period Factor = 365/365 = 1

Percentage = 365/ (1095-365)

= 365/730

= 0.5

For Year 2024

Period Factor = 366/366 = 1

Percentage = 366/ 365

= 1.002740

Depreciation = Base * Period Factor * Percentage

= 2401639 * 1 * 1.002740

= 2408219

Note:

- Calculated depreciation amount is more than the remaining amount to be depreciated. So, it has activated the “Amount Reduced” flag and made the depreciation amount as 2401639.

- While calculating percentage it has taken 366/365 and not 365/ 365 because the remaining life in 2024 is not more than a year

Scenario 3:

Useful Life: 5 Years

Base Method: Percentage from useful life

Depreciation to the Day: Activated

Depreciation start Date: 01/02/2020

For Year 2020

Period Factor = 335/366 = 0.91530

Percentage = 365/1825

= 0.2

For Year 2021

Period Factor = 365/365 = 0.91530

Percentage = 365/ (1825 – 335)

= 365/1490

= 0.244966

For the Year 2022 to 2024 the calculation is similar.

For the Year 2025

Period Factor = 31/365 = 0.08493

Percentage = 365/30

= 12.166667

Note: Here I have taken 30 days as remaining useful life while calculating Percentage because the calculation in SAP S/4HANA happens by considering the total days depreciated in the first year of acquisition. In this case 335 days has already been depreciated in 2020, so in 2025 it has considered 365-335 = 30 days for calculating percentage. But if you notice the calculation of period factor the days is still considered as 31.

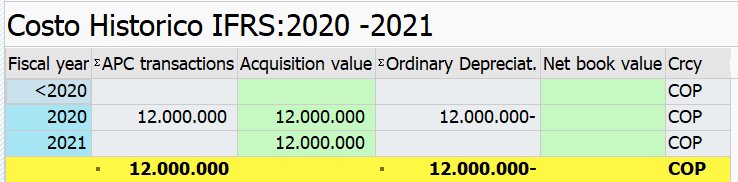

Scenario 4:

Useful Life: 1 Years

Base Method: Percentage from useful life

Depreciation to the Day: Activated

Depreciation start Date: 01/01/2020

For Year 2020

Period Factor = 366/366 = 1

Percentage = 366/366 = 1

Note: If the useful life is 1 year then the calculation will consider the leap year unlike the other scenarios where leap years are ignored. Here the days in Percentage calculation will be 366 days as 2020 being a leap year.

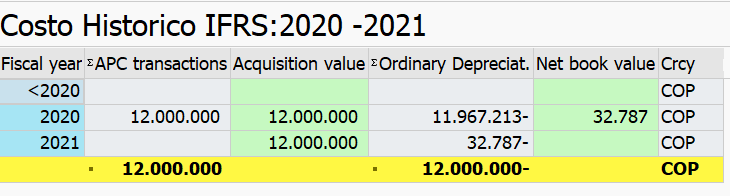

Scenario 5:

Useful Life: 1 Years

Base Method: Percentage from useful life

Depreciation to the Day: Activated

Depreciation start Date: 02/01/2020

For Year 2020

Period Factor = 365/366 = 0.99727

Percentage = 366/366 = 1

Note: The remaining amount will be depreciated in the year 2021 on 1st jan.

For Year 2021

Note: For the scenario 4 and 5, I have implemented a customized SAP Note given by the product team for our customer. In SAP S/4HANA standard depreciation engine, the scenario 4 and 5 will have a residual amount at the end of Useful life i.e. the NBV will not become zero at the end of useful life.

Scenario 6:

Useful Life: 1 Years

Base Method: Percentage from useful life

Depreciation to the Day: Activated

Depreciation start Date: 02/01/2023

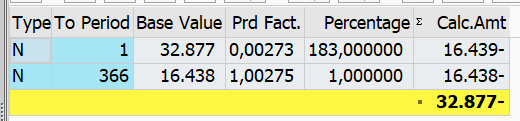

For Year 2023

Period Factor = 364/365 = 0.99727

Percentage = 365/365 = 1

For Year 2024

Period Factor = 1/366 = 0.99727

Percentage = 366/2 = 183

Note: Here it has considered 2 days while calculating percentage because 364 days has already been expired, but at the moment we reach year 2024 the useful life is 366 days. So, remaining useful life is calculated as 366-364 = 2 days.

Scenario 7:

Useful Life: 1 Years

Base Method: Percentage from useful life

Depreciation to the Day: Activated

Depreciation start Date: 01/03/2023

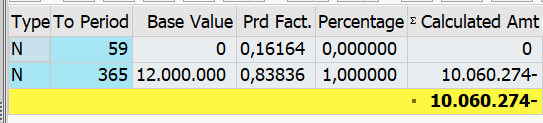

For Year 2023

Period Factor = 306/365 = 0.83836

Percentage = 365/365 = 1

For Year 2024

Period Factor = 60/366 = 0.16393

Percentage = 366/60 = 6.1

Note: Here it has considered 60 days while calculating percentage because 306 days has already been expired, but when we reach year 2024 the useful life is 366 days. So, remaining useful life is calculated as 366 – 306 = 60 days.

Scenario 8: Addition

This scenario covers the posting of additional acquisitions

Useful Life: 10 Years

Base Method: Percentage from useful life

Depreciation to the Day: Activated

Depreciation start Date: 01/01/2020

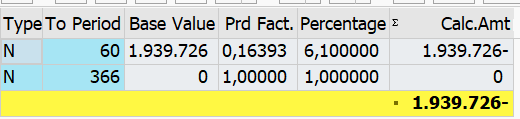

For Year 2020

1st Acquisition – 1/1/2020 for value 12000000

2nd Acquisition – 1/4/2020 for value 20000000

Note: The acquisition value of 12000000 on 1/1/2020 will be depreciated for 91 days i.e until the 2nd acquisition on 1/4/2020.

On 1st Acquisition

Base Value = 12000000

Period Factor = 91/366 = 0.24863

Percentage = 365/3650 = 0.1 (As explained in earlier scenarios the value 3650 is obtained by calculating 10*365)

On 2nd Acquisition

Base Value = 12000000 – 298361 + 20000000

= 31701639

Period Factor = (366 – 91) / 366

= 275/366

= 0.75137

Percentage = 365/ (3650-91)

= 365/3559

= 0.102556