Introduction

This article aims to covers the set up involved in Asset Accounting and its interaction with the General Ledger module. The article aims to cover intricacies involved with respect to Asset Accounting to minimize the challenges faced during the set-up.

Note: The article does not cover the migration aspects involved while moving to Asset Accounting.

The usage of Asset Accounting is not just restricted in S/4 HANA. It can be used with ECC system also (from EHP 7 onwards), provided New GL is activated. However, the difference is while it is mandatory to activate new Asset Accounting in S/4, it is an optional feature in ECC. Additionally, AA in S/4 provides additional features that are not available in ECC.

Before configuring Asset Accounting, it is important to list out all the accounting principles that the organization desires to follow while preparing its financials and to determine whether each of these accounting principles would translate into separate parallel ledgers.

Once this has been determined then, it becomes easier to proceed with the next steps.

Set up of Asset Accounting

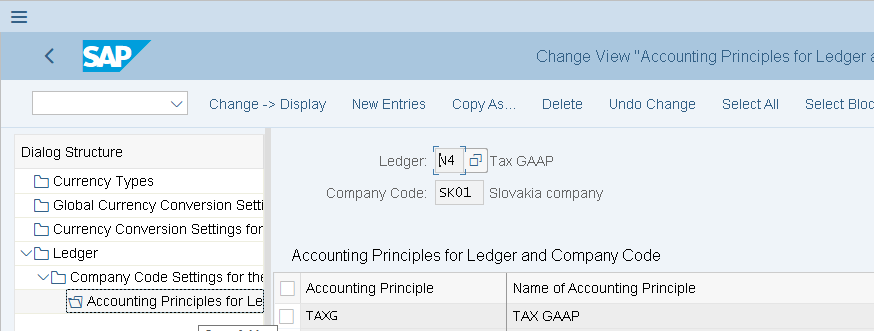

Let us assume that an entity is required to follow the IFRS for its Financial Reporting as per statute. Additionally, it needs to have a tax reporting and local reporting in place….

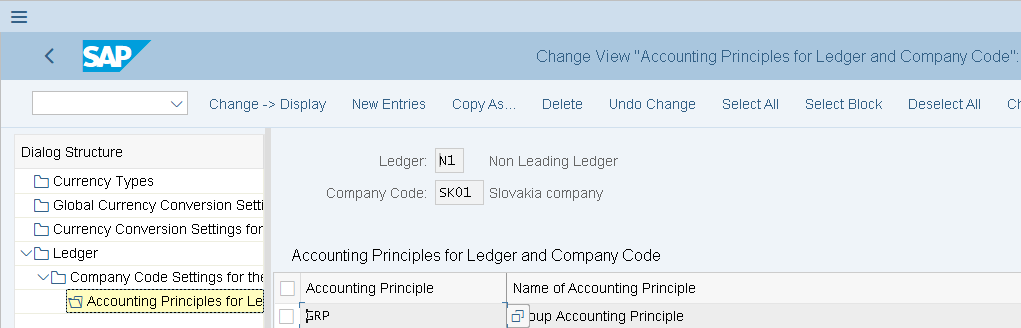

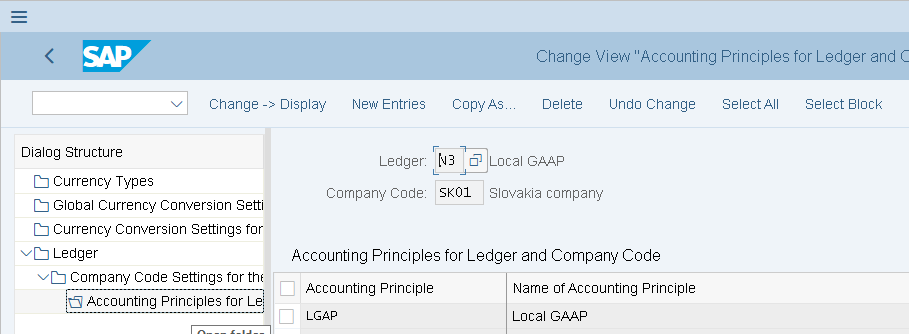

The entity would in this case set up its Leading Ledger 0L in consonance with the IFRS. Three parallel non-leading ledgers need to be set up in accordance with the Taxation, Group Reporting and Local GAAP Requirements. Accordingly, Ledger 0L has been set up for IFRS purposes and Ledgers N1, N3 and N4 for Group Local and Taxation Requirements respectively.

See the below set up:

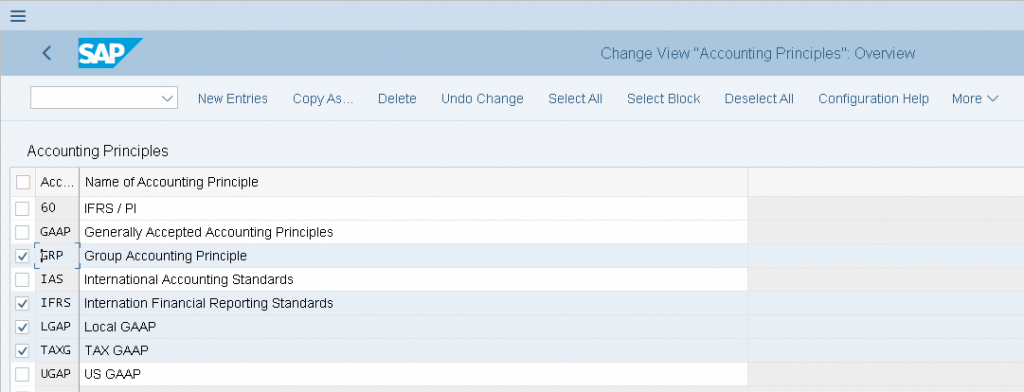

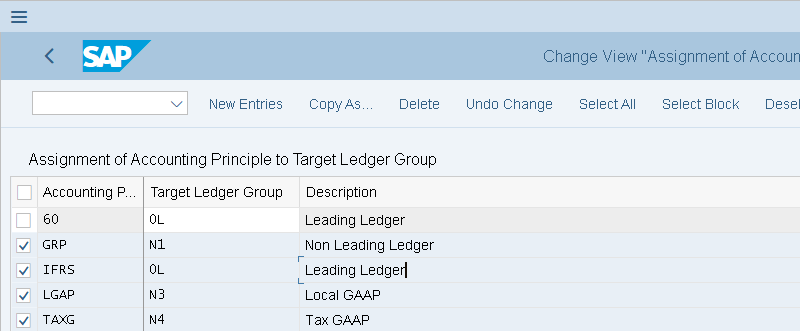

We have defined four accounting principles as follows in the below path:

Financial Accounting-Financial Accounting Global Settings-Ledgers-Parallel Accounting-Define Accounting Principles:

Thereafter we have defined the ledgers and the accounting principle they represent:

IFRS Ledger-Leading Ledger

Group Ledger-Non-Leading Ledger

Local Ledger-Non Leading Ledger:

Tax Ledger-Non Leading Ledger

We have also assigned accounting principle to Ledger Group:

Financial Accounting-Financial Accounting Global Settings-Ledgers-Parallel Accounting-Assign Accounting Principles to Ledger Groups:

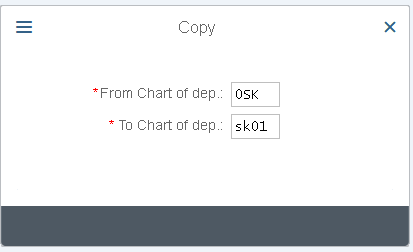

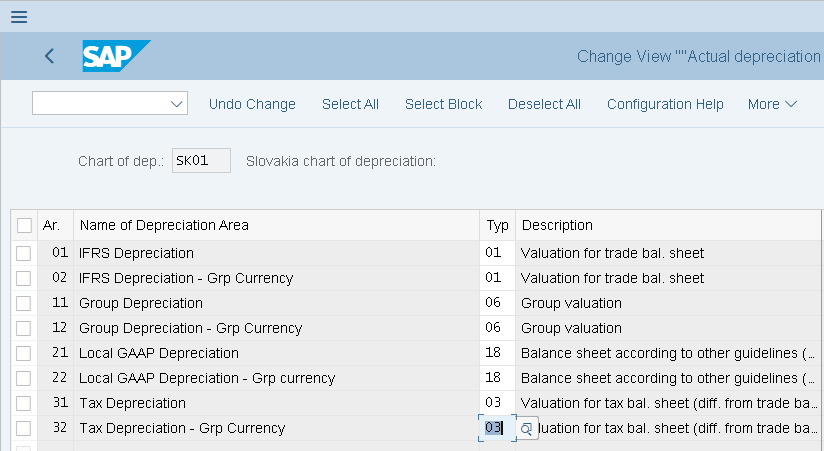

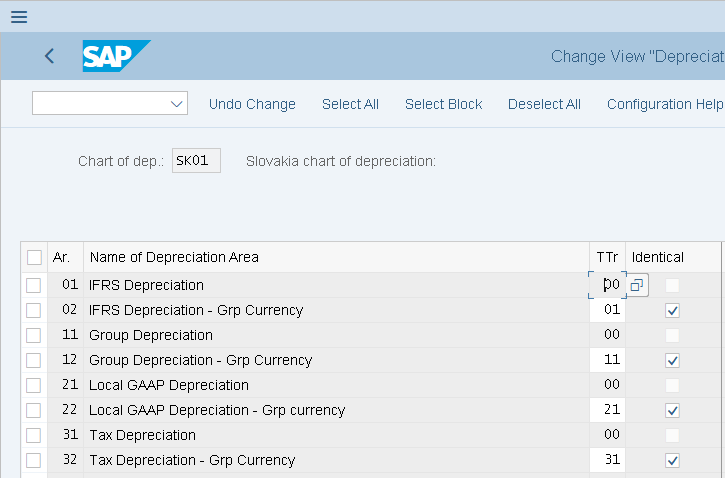

Once the ledger and accounting principle set up is complete, we set up the Chart of Depreciation. In this example we are copying the new Chart of Depreciation SK01 from 0SK:

Financial Accounting-Asset Accounting-Organization Structure-Copy Reference Chart of Depreciation:

Once the Chart of Depreciation is copied, we rename the same and delete all the depreciation areas:

Financial Accounting-Asset Accounting-Organization Structure- Specify Description of Chart of Depreciation/ Copy Delete Depreciation Areas

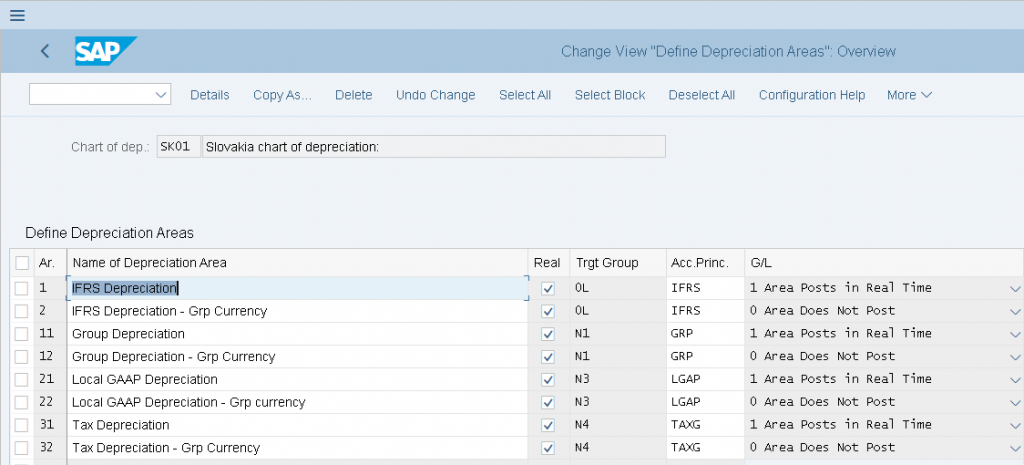

In our case we have set up four depreciation areas namely IFRS, Group Valuation, Tax GAAP and Local GAAP. Before we finalize the depreciation areas, the following points must be considered.

1. The depreciation area must specify the type or purpose of depreciation. This is done under the following path:

SPRO-Financial Accounting-Asset Accounting-General Valuation-Depreciation Areas-Define Depreciation Areas-Specify Area Type

Here we have defined book depreciation for the purposes of Valuation for trade valuation, Tax depreciation for taxation requirements and likewise.

2. The input and output tax indicators need to be set up for the company code. This is an essential pre-requisite to the set-up:

SPRO-Financial Accounting-Asset Accounting-Integration with General Ledger Accounting-Assign Input Tax Indicator for Non-Taxable Acquisitions

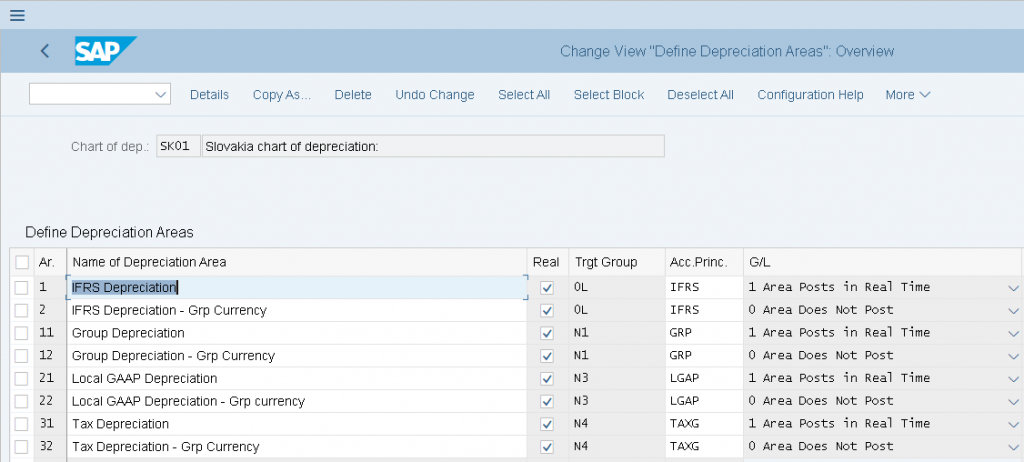

3. Traditional asset accounting does not require every depreciation area to be assigned to a ledger group. However, in new Asset Accounting each depreciation area must be assigned to a ledger group. This is a mandatory step in New Asset Accounting. The ledger group might/might not post. However, each area must be assigned to a ledger group.

4. In Asset Accounting (new), the system must ensure that all ledgers in which the company code updates its balances in the GL module are also updated via Asset Accounting. Here all the four ledgers in which the company updates its balances, namely 0L, N1, N4 and N4 also post real time via Areas 1, 11, 21 and 31. Also all representative ledgers assigned to the ledger groups used in the assigned chart of depreciation must also be assigned to the company code.

5. In new Asset Accounting, for every currency type in company code, we need to create parallel depreciation area for each of our accounting principle that does not post to G/L. Since the company code in our example had a parallel currency defined, we needed to create an additional area that does not post. So, we create four new areas, namely 2, 12, 22 and 32 each representing an accounting principle defined earlier that does not post.

6. Unlike in traditional asset accounting where only one ledger group can post in real time, in new Asset Accounting multiple ledger group can post in real time. On account of this reason, the need for delta depreciation area and the periodic APC transaction posting RAPERB2000 is no longer needed in New Asset Accounting.

7. A depreciation area cannot be mapped to an extension ledger. The ledger must be standard ledger.

8. A depreciation area cannot be mapped to an extension ledger. The ledger must be standard ledger.

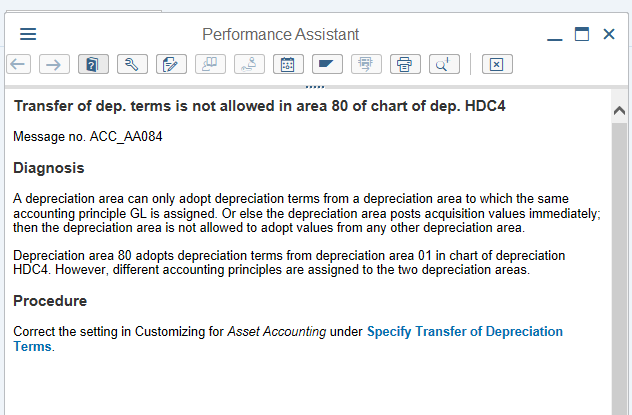

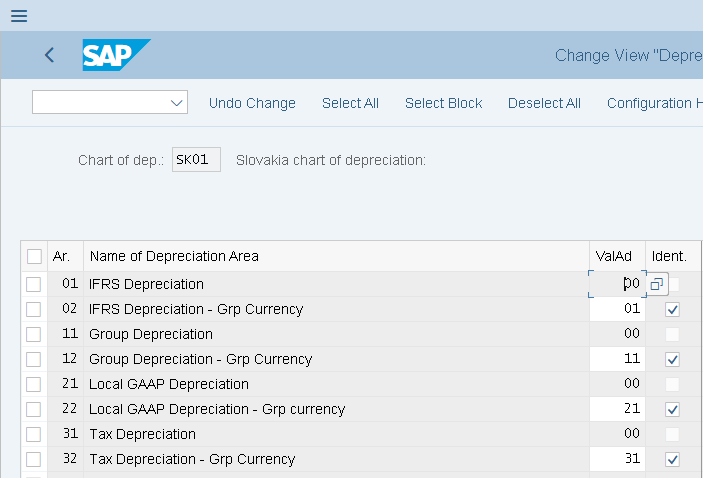

In our example each of the depreciation areas 01, 11, 21 and 31 represent a different accounting principle and hence they need cannot adopt values from other depreciation areas.

See setting below:

Financial Accounting-General Valuation-Depreciation Areas-Specify Transfer of APC values

Financial Accounting-General Valuation-Depreciation Areas-Specify Transfer of Dep Terms

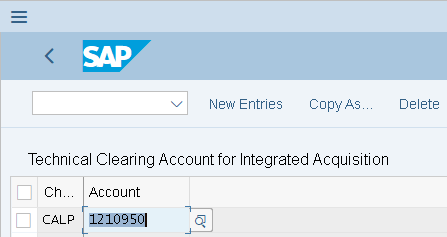

Set up of technical clearing account in new Asset Accounting

New Asset Accounting requires a technical clearing account to be set up. The system divides the acquisition posting into two parts, the operational and the valuating part.

- The operational part pertains to the vendor invoice which is ledger group independent document i.e. posts to all the ledgers (valid for all accounting principles).

- The valuating part pertains to posting capitalization of the asset. This document is ledger group dependent document. This is valid only for a given accounting principle

- Both the operational and the valuating part are posted against the technical cleating account. The technical clearing account is defined in the following set up

Financial Accounting-Asset Accounting-Integration with General Ledger Accounting-Technical Clearing Account for Integrated Asset Acquisition-Define Technical Clearing Account for Integrated Asset Acquisition

The technical clearing account needs to be defined as Reconciliation for Asset and due to the operational and valuating part of the posting, for each accounting principle in the Chart of Depreciation the balance in this account would be zero.

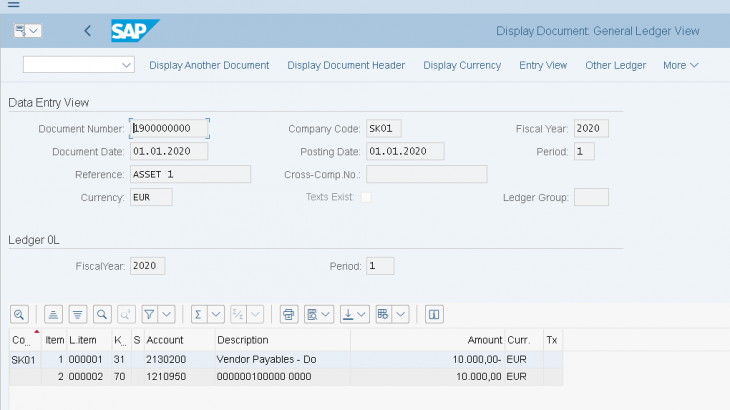

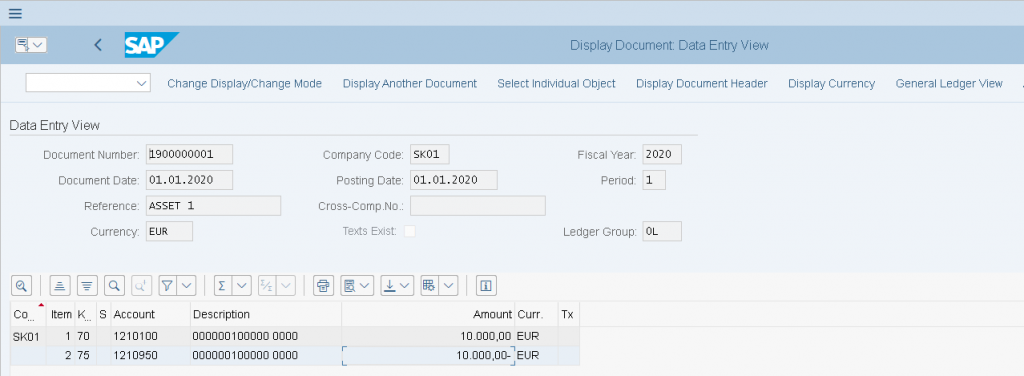

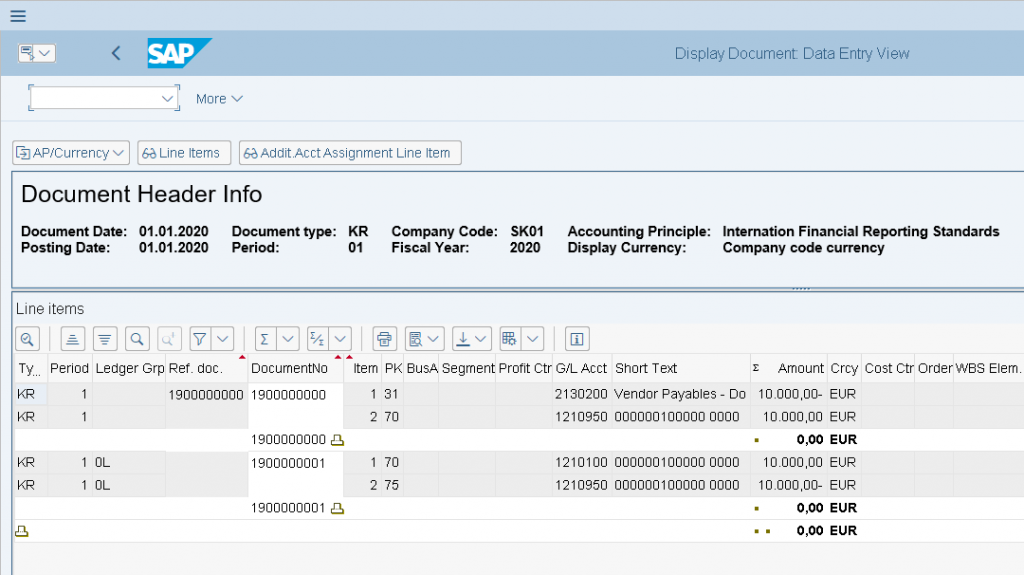

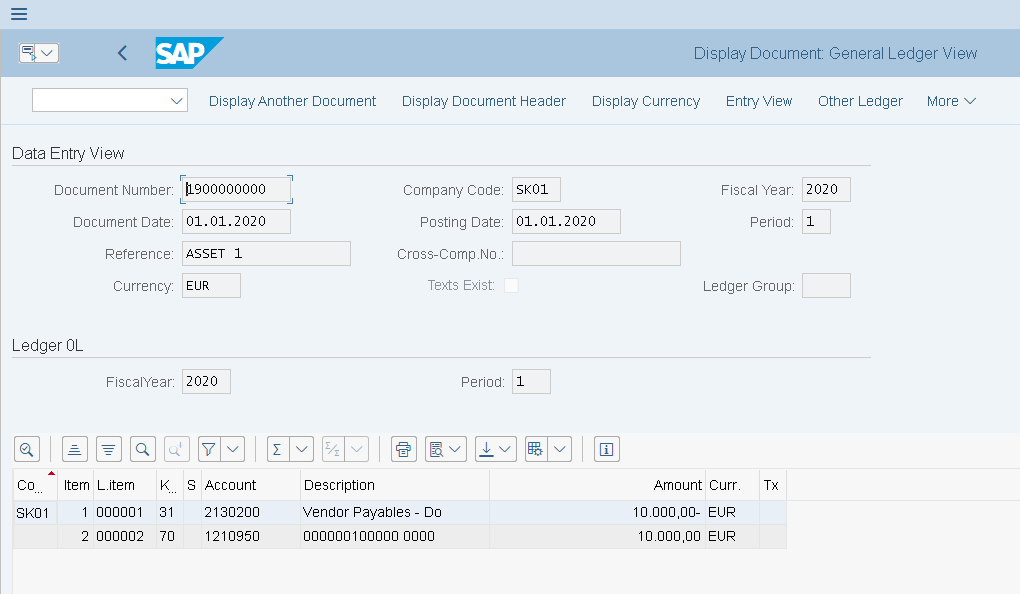

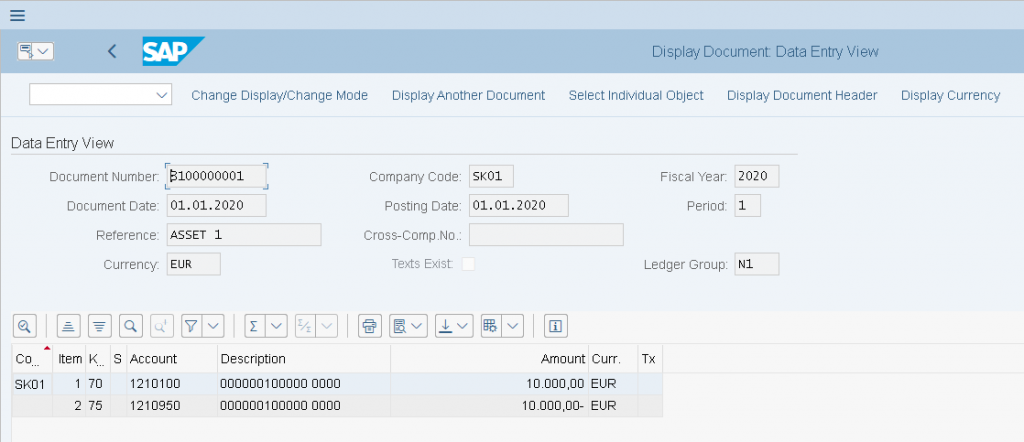

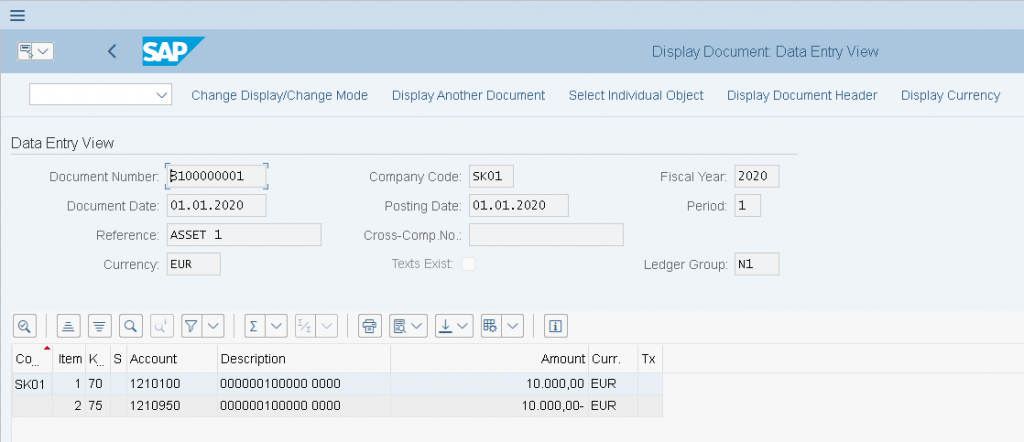

Example of an acquisition posting:

Checking the Asset View- Operational and Valuation Part:

The first part is the Operational part and the second part is the valuating part

Operational Part:

Valuating Part in 0L:

Valuating Part in Ledger N1:

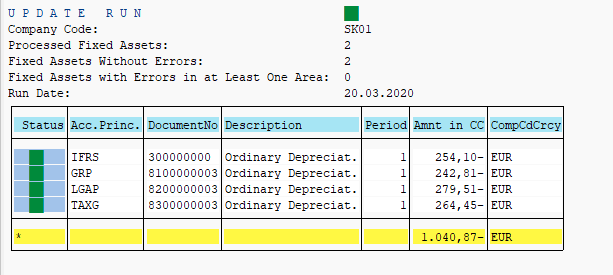

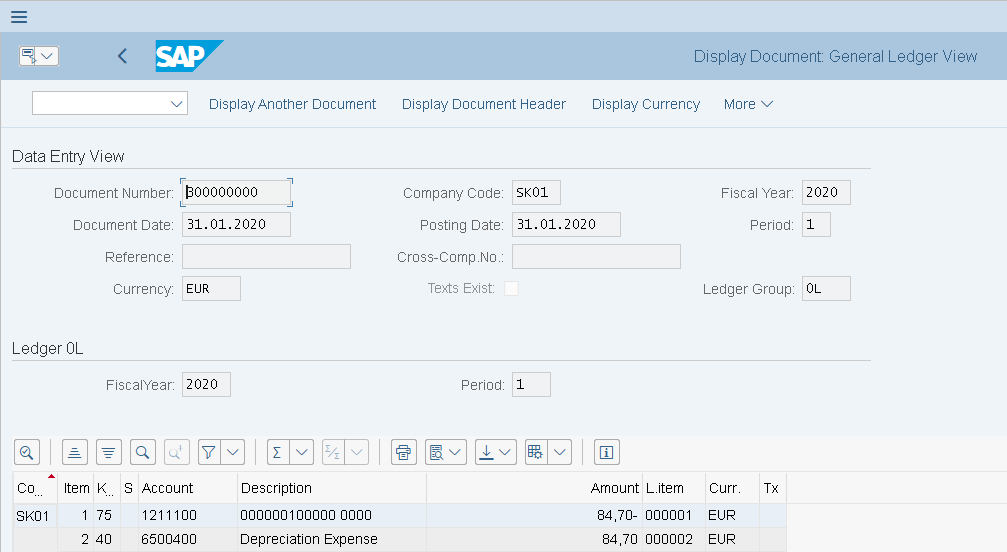

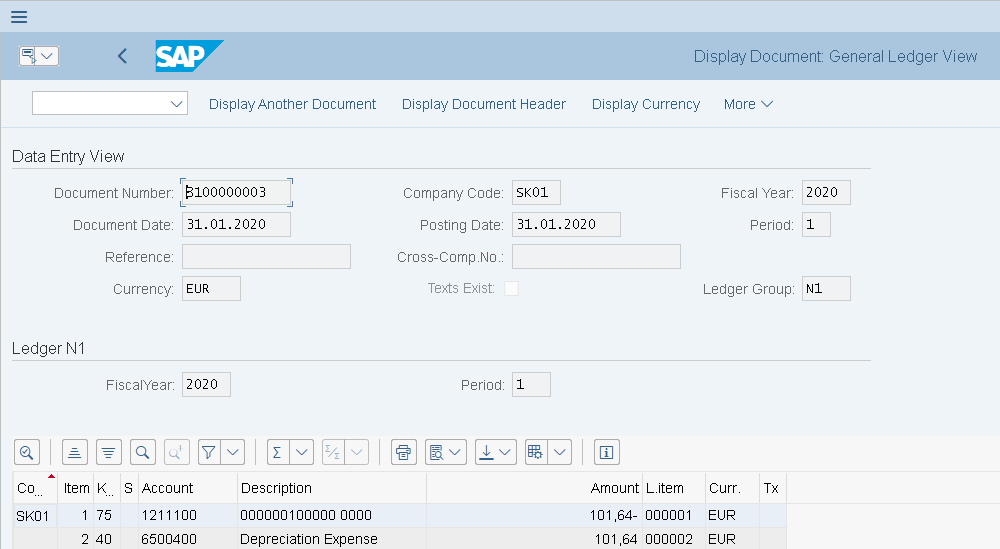

Depreciation Run postings in each ledger:

Ledger 0L:

Ledger N1:

Similarly document for depreciation will be posted in all the non-leading ledgers.

Note: The company code used here is a dummy co code.